USPS Pensions vs. the World: More Rules, Worse Funding

The United States Postal Service (USPS) holds a special place among the world’s mail carriers. It moves more mail and generates more revenue than anyone else, with one of the largest postal workforces on the planet. But being the biggest isn’t cheap, and the USPS faces more rules than foreign carriers ever have to deal with. Nowhere is this divide more visible than in the Service’s attempts to pay for the retirement benefits it promises to workers.

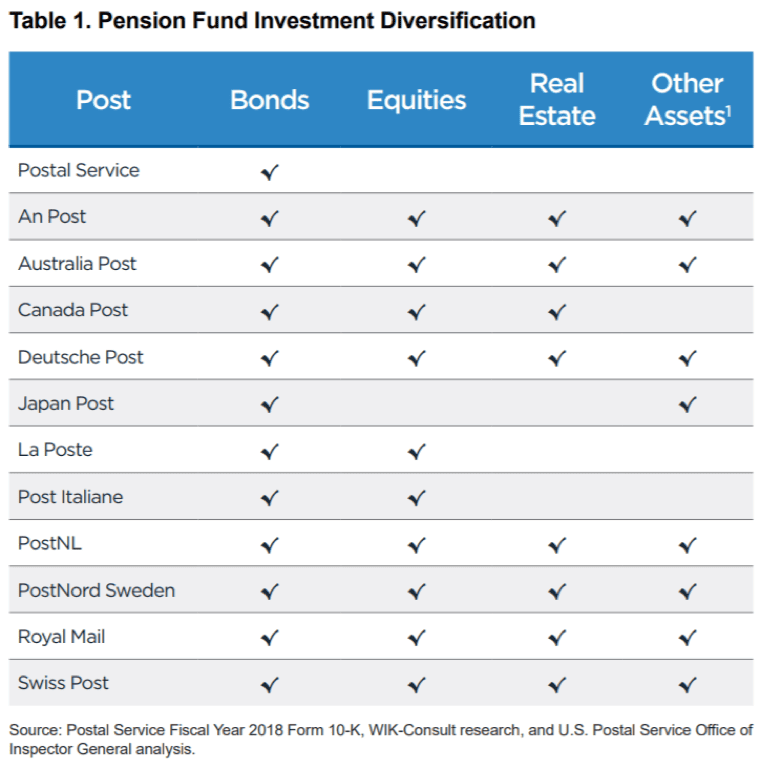

In a new white paper, the USPS inspector general’s office (OIG) compares America’s governance of postal pension benefits to peer agencies in other developed economies. The report notes a few key differences between the USPS and these other postal services, the foremost being the American agency’s prohibition on diversification of its investment portfolio. As the table below illustrates, USPS pension funds are invested solely in bonds, specifically special-purpose, low-risk treasury bonds created specifically for postal savings. Different rules apply to investment of pension savings for other federal workers. But limited risk and no diversification also means limited potential return when the economy grows.

As we can see, the USPS is unique in its apprehensive investment strategy. The OIG explains that, “Unlike the Postal Service, the 11 foreign posts generally base the financing of their pension plans on sophisticated portfolio and risk optimization, attempting to capture opportunities in capital markets at home and abroad.” That said, bonds still form the preponderance of most postal pension investment portfolios, with the balance spread across investment types. Low-risk assets make a lot of sense for self-funding mail companies, limiting pressure for taxpayer bailouts when global economic downturns damage government balance sheets.

The problems with extra-conservative investment rules arise when postal finances are weak and pension plans go underfunded. Conversely, taking on extra investment risk during economic expansions can help mail agencies close funding gaps left by failures to save enough to pay future retirees.

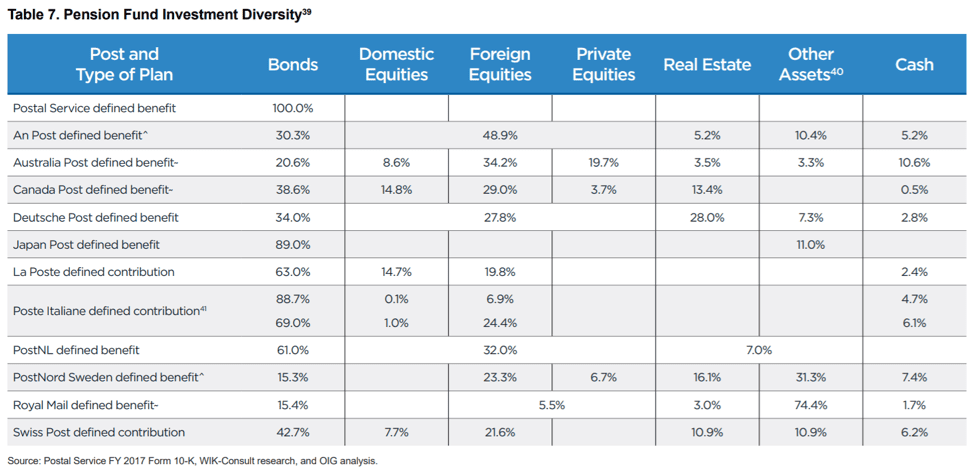

This problem is particularly acute for the USPS, whose pension plan funding levels are worse than peer agencies. Despite having more than $278 billion in assets, USPS pensions are underfunded by more than $40 billion. Only Japan Post comes anywhere close to this level of underfunding, holding a shade under $20 billion in liabilities to its retirees.

In a previous report from 2017, the OIG noted that easing the mandates that force USPS pensions to be invested in special-purpose treasuries could almost completely close the pension funding gap with greater returns on what the agency has already saved.

The new study showcases other countries’ postal pension savings investment models, providing a multitude of options should Congress make changes to shore up the agency’s shaky finances. In Table 4 (not shown), it lists the fiduciary rules that apply to pension investments in each country studied, all of which allow investment options legally unavailable to the USPS.

Notably, no other major country studied has special laws to restrict the scope of postal pension investments. Rather, they have blanket rules for pensions that apply to “other employees and pension funds in their respective countries.” Many mandate that pension funds hold a diverse portfolio of assets, the exact opposite of the rules that bind the USPS.

Countries like Canada and Australia have been leaders in pension fund diversification for decades, with broad discretion to invest in assets that will yield appropriate returns. Funds in both nations have been rewarded with returns on assets in an array of countries and industries. Other countries place some guardrails on pension fund investment, like Italy’s rules that bar investment in real estate or Ireland’s rules that require more than half of investments to be in “regulated markets.”

The facts of the OIG report paint a picture of an agency held back by special rules that treat its workers differently from other federal employees to the detriment of both the USPS and its workforce. Moving to a broader system that reconciles the differences between how the USPS invests pension savings and how the government at large invests savings for other federal workers would benefit every substantial postal constituency. $278 billion in investments could buy plenty of diversity to insulate the USPS from economic downturns, if Congress ever lets it buy something other than bonds.